|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

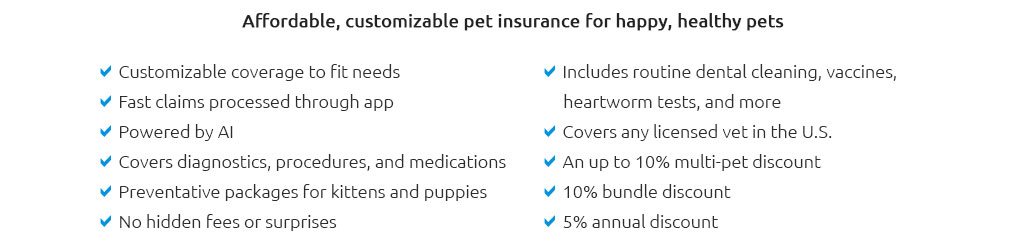

dogs pet insurance decisions guided by proof and controlPredictable vet costs and the ability to approve care without guessing the bill. That is the practical role of coverage, not magic. What it is and how it fitsIt's a reimbursement contract for eligible veterinary expenses. You pay premiums; the insurer pays a percentage of approved costs after your deductible, up to a policy limit. No provider networks in most cases, so any licensed veterinarian can be used. Coverage building blocks

Common exclusions and limits

Proof via quick math

Control levers you set

Costs and how to forecastPremiums vary by breed, age, and ZIP. Younger mixed-breed dogs may land around $25 - $60 per month; large or pure breeds can exceed $90; seniors can exceed $150. Expect annual increases tied to rising vet costs and the dog's age. A real-world moment11:10 pm. Lab mix swallowed a sock. ER estimate: $2,200 for imaging and endoscopy. Policy: 90% reimbursement after a $250 annual deductible. I authorize treatment immediately. Eligible amount $2,200 minus the $250 deductible leaves $1,950; insurer pays $1,755; my out-of-pocket is $445. The claim closed in five days, funds landed via direct deposit. Proof beats guesswork. How to pick without regret

Realistic-checkAsk your vet for itemized invoices and treatment notes; insurers need line items to adjudicate. Keep records in one folder. Waiting periods apply - don't expect day-one illness coverage. If surgery is scheduled, request a pre-claim estimate; emergencies typically don't wait for pre-approval. Alternatives and complements

Bottom lineUse insurance to convert uncertain, potentially large vet bills into planned costs. Choose deductible, reimbursement, and limits that fit your tolerance for risk. Track results with simple math, keep documentation tidy, and you stay in control.

|